Please find below a pdf file containing the TDS rates and limits applicable for FY 2021-22 /AY 2022-23.

TDS RATES FY 2021-22

Please find below a pdf file containing the TDS rates and limits applicable for FY 2021-22 /AY 2022-23.

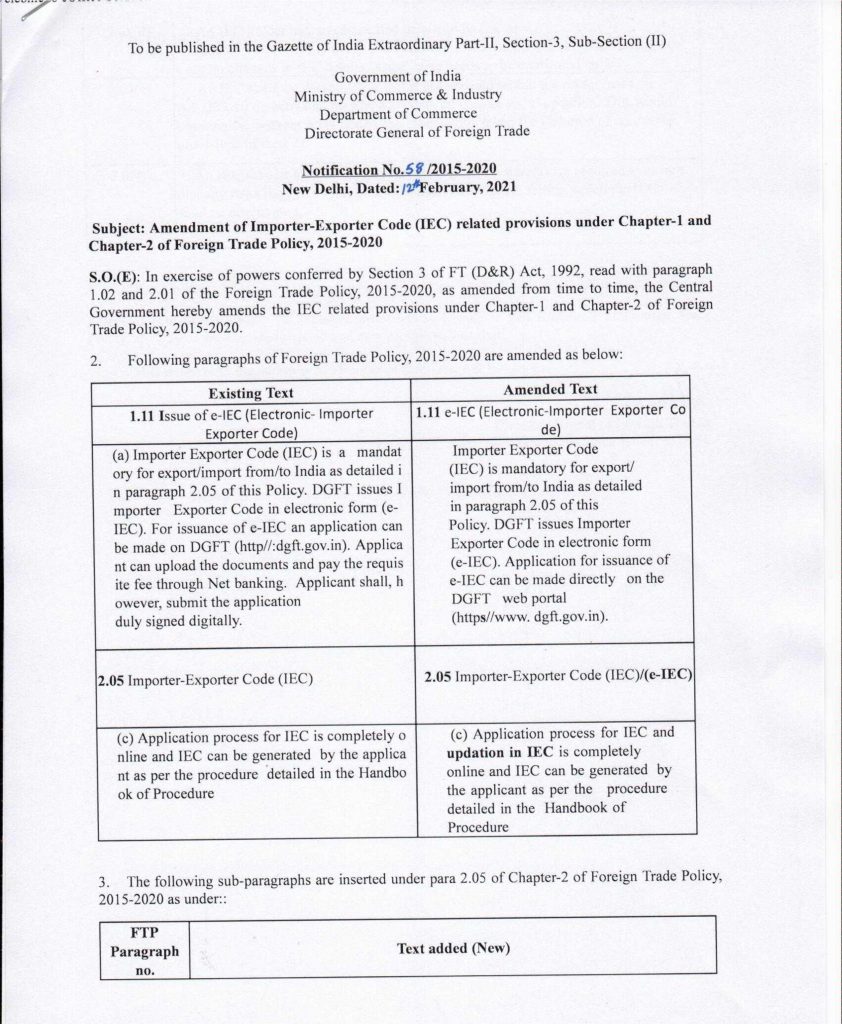

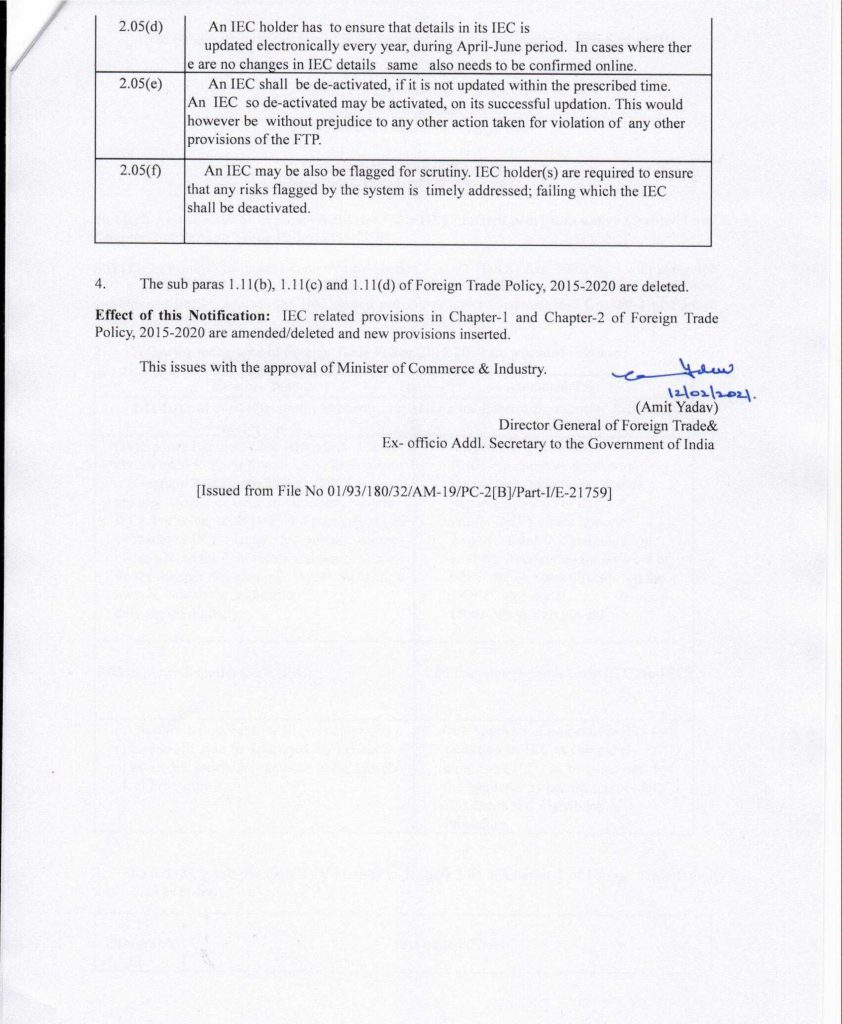

The Central Government has amended the rules relating to Importer-Exporter Code (IEC) vide Notification No. 48/2015-2020 dated 12 February 2021.

The notification has introduced additional compliance of a yearly updation of the IEC on importers and exporters, to be done in the months of April – June. A confirmation would be required even if there are no updates/changes to the IEC.

In the event the updation activity is not done within the prescribed time by a business, the same will be deactivated without prejudice to other actions in law, including under the Foreign Trade (Development & Regulation) Act, 1992.

This additional requirement should be carefully adhered to by businesses, as any non-compliance will result in a deactivation of the IEC and a stop to all import-export activity resulting in severe business losses.

The notification copy is below:

What is Hindu Undivided family?

Hindu undivided family (HUF) is a Joint Hindu family with common ancestors. The Hindu Succession Act, defines a HUF, as a family of persons lineally descended from a common ancestor and related to each other by birth or marriage.

In other words, three conditions need to be satisfied:

Who can be the Karta, Coparcener or a Member of an HUF?

Karta is the person who manages or represents the HUF and is generally the senior-most male member of the family. Only a Co-parcener can become the Karta of HUF.

Any person (male or female) born in a Joint Hindu family who is within four degrees in lineal descendent from the common male ancestor is considered as a coparcener and anyone who becomes part of the family by virtue of marriage is treated as a member. However, a person who is adopted into the family also becomes its coparcener from adoption though not born in the family. As per the amended law since 2005, even a girl child becomes a coparcener by birth and can continue to be a co-parcener of her father’s HUF even after her marriage. However, she will only be a member of her husband’s HUF.

Co-parceners have a right to seek partition and become the Karta of the HUF. Whereas, Members have the right to be maintained out of the funds of HUF, and receive their share at the time of partition but do not have the right to seek for partition or become the Karta.

How taxed under Income tax Act.

The Income-tax Act recognizes such family as a separate entity. The definition of ‘person’ under section 2(31) of the Income Tax Act 1961 includes HUF as a separate person having its own status, distinct from any individual, firm, company, etc. A HUF is created by the operation of law and therefore cannot be created by the actions of a person.

How to create a HUF

HUF comes into existence automatically at the time of marriage. It is created through executing a deed, obtaining PAN, and applying for a bank account. The various source of its assets could be:

Note: To ensure personal assets or funds are not transferred to HUF account as income generated from such assets/funds will attract clubbing provisions.

How creating of HUF helps save tax legally

HUF is considered a separate legal entity as per law and hence has its own PAN and files tax returns independent of its members. By forming a HUF, one can optimize their tax liabilities and also include their family members to benefit in the future. The various advantages are:

A HUF is taxed at slab rates – the same rate as that of an individual and is eligible for a basic tax exemption limit of Rs 2,50,000.

HUF is also separately eligible for various deductions under section 80 such as:

Thus, total deduction of Rs 1,90,000 could be availed by the HUF irrespective of its individual member deductions.

Further specific deductions on medical treatment/expenditure of disabled or dependent family members, donations to charity, etc can be availed based on the amount spent for the said purposes.

The HUF can carry on certain family business like any other entity:

The HUF is permitted to invest in various tax-free instruments. Also, it can avail specific capital gain exemptions under sections 54, 54B, 54F, 54EC, etc., and optimize its tax liabilities for the benefit of the entire family.

The sole purpose of the family settlement should be to settle existing or future disputes regarding property, amongst the members of the family. Since this arrangement does not involve the transfer, it would not attract gift tax, capital gains tax, or clubbing. In a family arrangement, tax incidence is considerably reduced or it may even become nil.

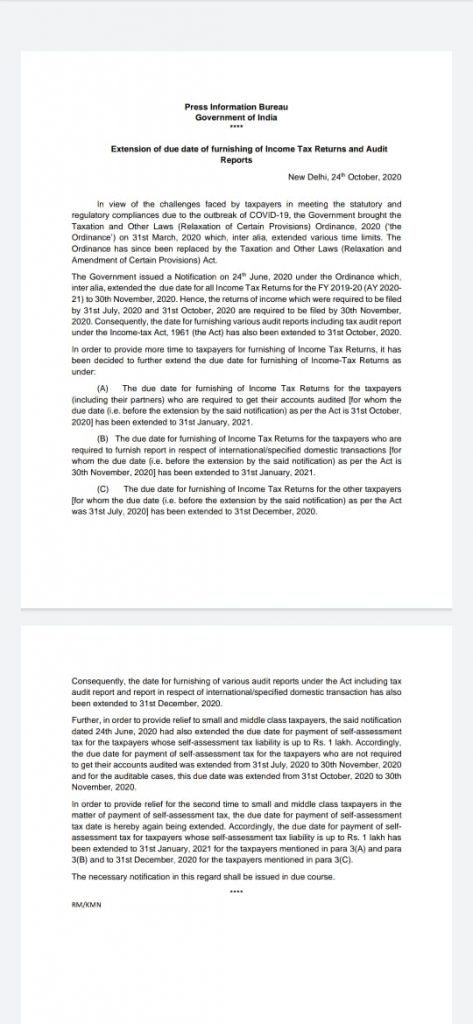

1. The due date for furnishing of Income Tax Returns for taxpayers (including their partners) who are required to get their accounts audited [for whom the due date (i.e. before the extension by new notification) as per Income Tax Act is 31 Oct 2020] is extended to 31 Jan 2021.

2. The due date for furnishing audit reports including tax audit report & report in respect of international/specified domestic transaction extended to 31 Dec 2020.

3. The date for payment of self-assessment tax for those with self-assessment tax liability of upto Rs.1 lakh extended to 31 Jan 2021.

4. The due date for furnishing of Income Tax Returns for the other taxpayers [for whom the due date (i.e. before the extension by the said notification) as per the Act was 31 July, 2020] has been extended to 31 December 2020.

Source: Press Information Bureau

A well-planned sale of property could save you from hefty taxes. The first and foremost critical aspect while selling a house to be kept in mind is the time for which the property has been held. The period of holding determines the benefits that are available and the exemptions that can be utilized to eventually determine the tax outflow.

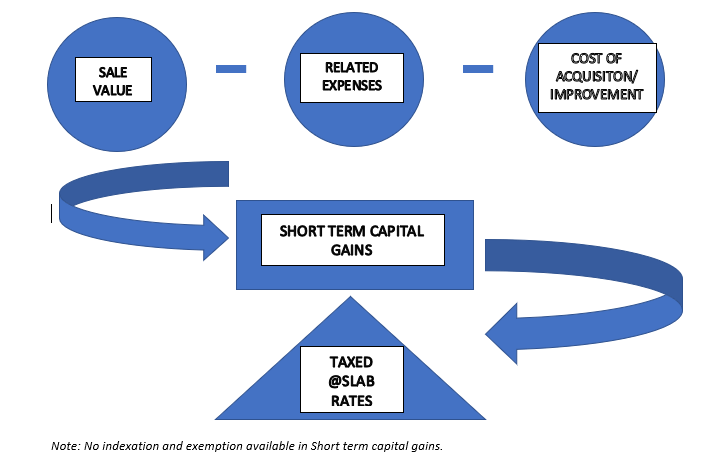

Property held for less than two years – tax implications

The sale value of the property, reduced by related sale expenses and cost of acquisition or improvement incurred is the resultant capital gains earned from the property. Such profit earned from the property which is held for less than two years will be subject to Short Term Capital Gains (STCG). The STCG on sale of the property is added to the total income of the seller and is taxed at normal slab rates applicable to such an individual. To understand better, those earning more than 10 lakhs a year would shell out 30% tax on such profits from the sale of property. Neither benefit of inflation index can be taken, nor any exemption for the investment of the profits be utilized to reduce the tax burden.

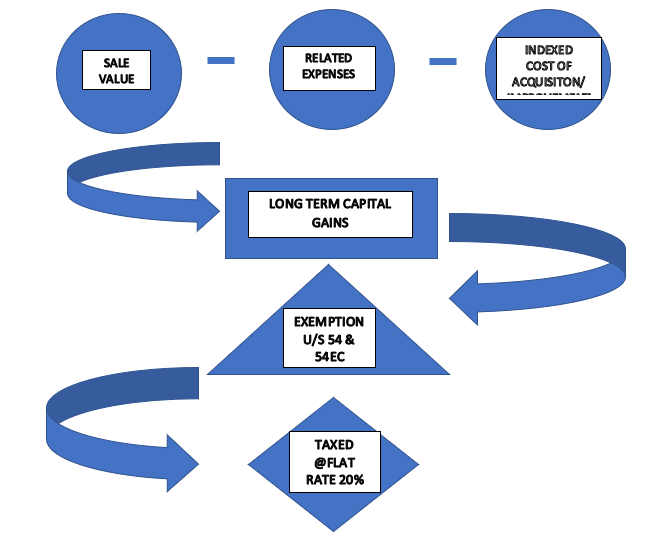

Property held for more than two years – tax implications

On the other side if the property is held for a period beyond two years the profit would be subject to tax at a flat rate of 20% after indexation. While computing such profits, the cost inflation indexation benefit would be given for the period held. Indexation takes into account the inflation for the period held and thereby adjusting the cost of acquisition.

Also, in case of longterm capital gains the seller can avail the various investment options available and claim exemption from payment of taxes. The various re-investment options available are as follows:

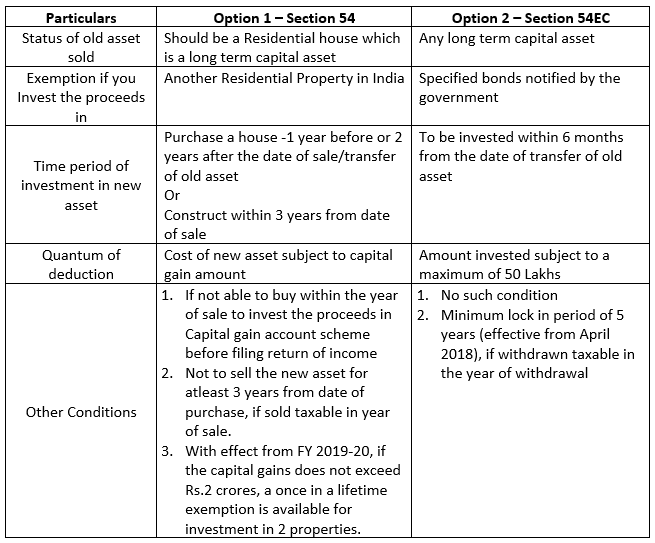

Exemptions and conditions

There are two exemptions which can be utilized by the person selling a house property to save himself from hefty taxes, they are as follows:

The Indian Trust Act, 1882, governs a Private Trust. Private trust is a vehicle through which property can be transferred from one person (owner) to another for the benefit of an individual or an ascertainable group of people.

A private trust is created for the benefit of specific individuals i.e., individuals who are defined and ascertained individuals or who within a definite time can be definitely ascertained. A family trust set up to benefit members of a family is the most common purpose for a private trust. The purpose of the family trust is for the settlor to progressively transfer his assets to the trust, so that legally the settlor owns no assets himself, but through the trust, beneficiaries get the benefit of these assets.

Private trusts can act an effective estate planning tool if you have a special child, a large business to be transferred to the next generation or a large estate to protect. Although the formation of a private trust resolves many issues, a lot needs to be considered in making a private trust, especially from the taxation point of view. As the income of a trust is taxed differently in different structures, careful planning is required to reap benefits without draining much money in the form of income-tax.

As the income of a private trust is available only to the beneficiaries, taxation is carried out according to the structure in which the income has been received.

From tax point of view, there are two structures under which the income of a private trust is taxed:

Specific trust: Here the income is received by the representative assesses on behalf of a single beneficiary. As the individual share of the beneficiary is known, taxation is done accordingly. For instance, it should be clearly stated in the trust deed that XYZ would get 50 per cent of the total income of the trust or the author’s son will draw the entire benefits from the trust.

Discretionary trust: With more than one beneficiaries, the individual shares are not known. Here the income of the trust is not received by a representative but determined by the trustees.

Taxability of Private Specific/Determinate Trust.

The Supreme Court in case of Nizams (supra) has held that

“It is also necessary to notice the consequences that seem to flow from the proposition laid down in s. 21, sub-s. (1), that the trustee is assessable” in the like manner and to the same extent “as the beneficiary. The consequences are three-fold. In the first place, it follows inevitably from this proposition that there would have to be as many assessments on the trustee as there are beneficiaries with determinate and known shares, though, for the sake of convenience, there may be only one assessment order specifying separately the tax due in respect of the wealth of each beneficiary. Secondly, the assessment of the trustee would have to be made in the same status as that of the beneficiary whose interest is sought to be taxed in the hands of the trustee….And, lastly, the amount of tax payable by the trustee would be the same as that payable by each beneficiary in respect of his beneficial interest, if he were assessed directly.”

Taxability of Private Discretionary Trust.

However, if the beneficiaries are carrying different status, then the status of the trustees cannot be determined. In such cases, the Courts have held that the trustees should be taken an assessable unit liable to be taxed as an individual (as discussed above).

Proviso to section 164(1) states that, in certain cases tax would be leviable as if it were the total income of an AOP. Proviso to section 164(1) only lays down that the rate of AOP would apply and it cannot be inferred therefrom that the trust would be considered as an AOP.

In so far as the private non-discretionary trust is concerned, the shares of the real owners of the income i.e. the beneficiaries is not known. Where the income of the trust accruing in a particular year is not distributed amongst the beneficiaries, one would not be aware about the income of any particular beneficiary. In such a case, the tax has to be paid by the trustee in representative capacity u/s 164(1).

In case where the income has been distributed to the beneficiaries, tax can be recovered from the trustee u/s 164(1). Further, in such cases, the Courts have held that the tax can be recovered from the beneficiaries also.

However, as already specified earlier there cannot be any double taxation.

Section 164(1) states that the income of an indeterminate trust would be taxable at MMR. Though it uses the word ‘charge’, section 164 does not create a charge [See Kamalini Khatau (supra)].

Proviso, to section 164(1) provides for exceptions to the above rate of MMR and in case of such exceptions, the rate applicable to AOP would apply.

If tax is recovered from the beneficiaries, it is doubtful whether the rates as applicable to the beneficiaries would apply or whether MMR would apply in accordance with section 164(1).

Further, section 161(1A) which provides for taxation of business income at MMR, would equally apply in case of indeterminate trust.

Also, as discussed earlier, special rates as are applicable to special income like long term capital gain would continue to apply.

Key Points

The various points to be kept in mind for tax planning purpose while opening a family trust are as follows:

a) It is applicable to all the sellers who are engaged in sale of goods. The term “seller” has been defined in the act.

b) The term “seller” means a person whose total sales, turnover or gross receipts from the business carried on by him exceeds Rs. 10 crores during the financial year immediately preceding financial year in which the sale of good is carried out.

c) Thus, the sellers who had a turnover/sales/gross receipts exceeding Rs. 10 crores in financial year 2019-20 will be required to collect TCS in financial year 2020-21.

d) If any person has turnover/sales/gross receipts below the above mentioned limit then it is out of scope of the term ‘seller’, meaning thereby the provision of this sub section shall not be applicable on that type of assessee.

e) The applicability criterion for TCS has to be considered & checked for every year

4. The provision of this subsection will not be applicable in the following circumstances:

The Annual General Meeting (AGM) due date for the financial year ended 31st March 2020 for all companies has been extended to 31st December 2020. A huge relief has been granted by the Ministry of Corporate Affairs by way of granting an extension of 3 months for holding the Annual General Meetings. Companies with the AGM due date of 30th September 2020 can conduct their AGM by 31st December 2020. The company is not required to file a separate application in form GNL-1 for an extension.