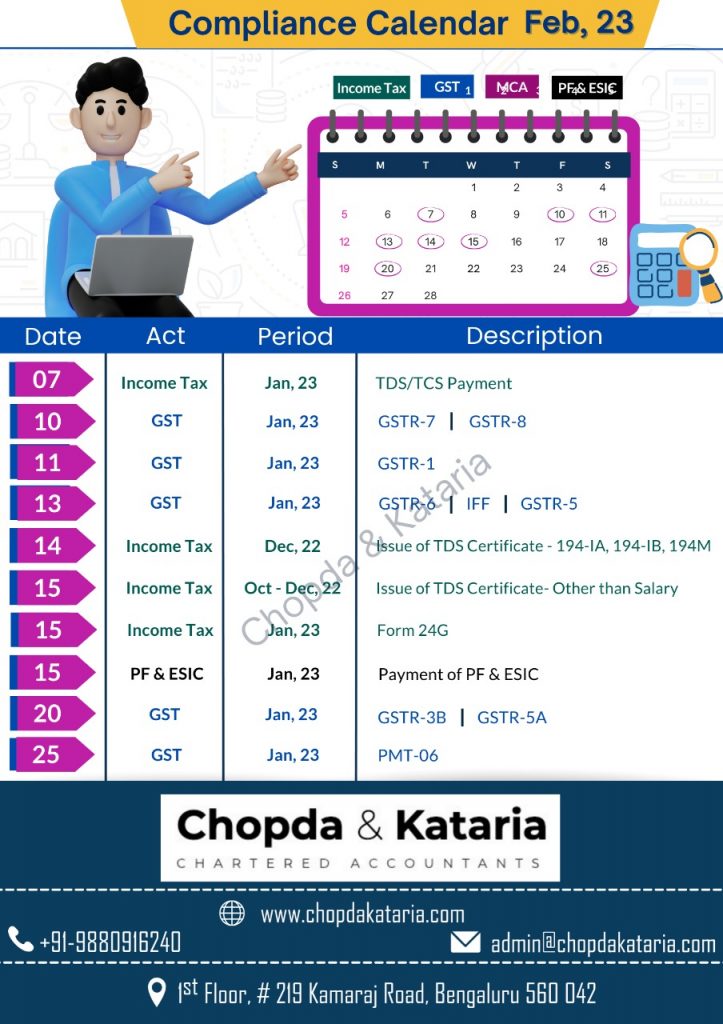

Compliance Calendar for February 2023

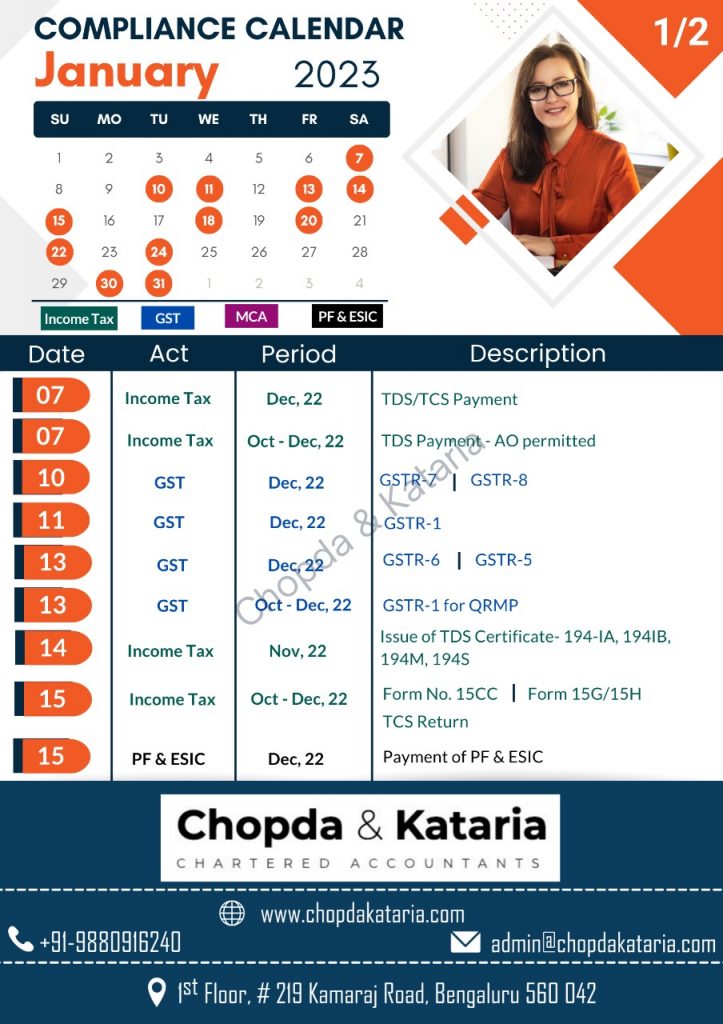

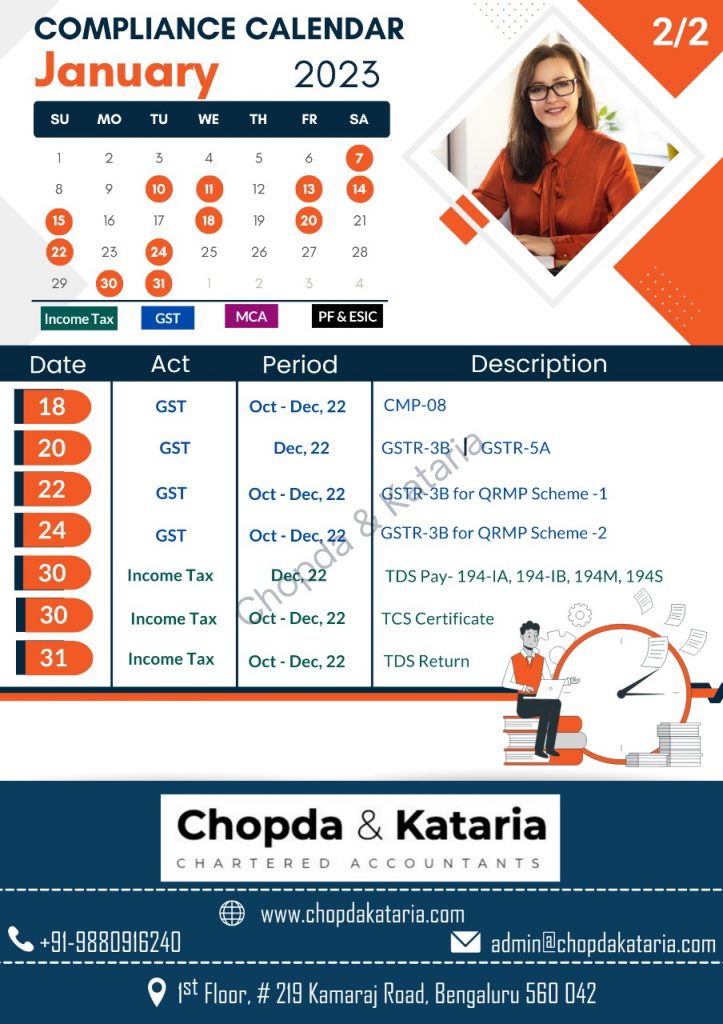

Compliance Calendar for January 2023

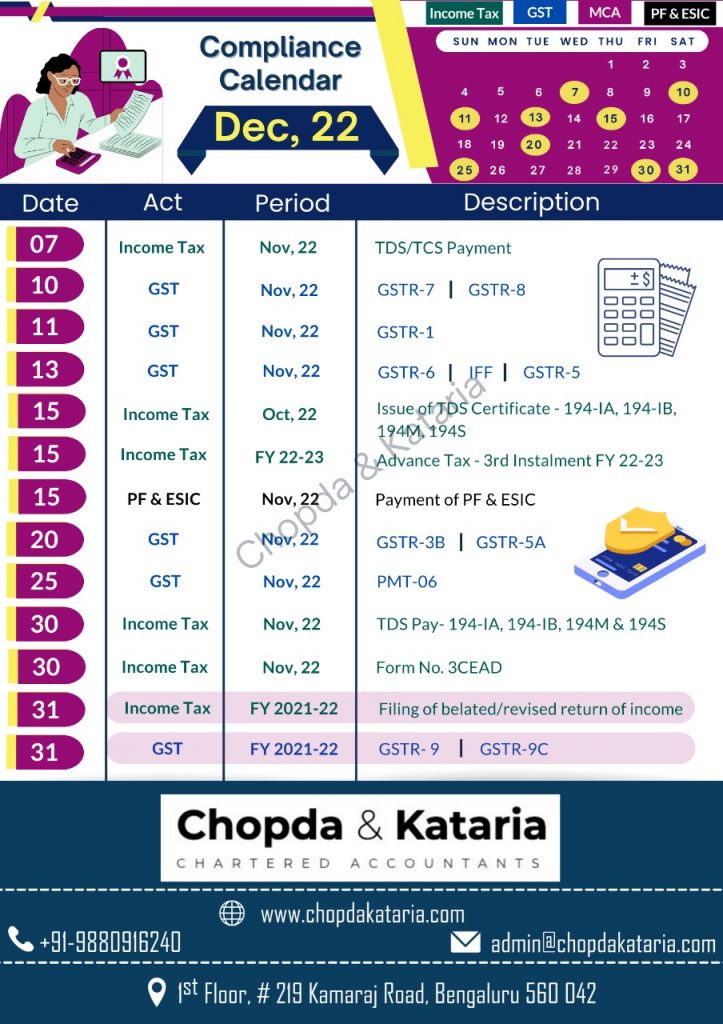

Compliance Calendar for December 2022

TDS Rates and Limits for FY 2022-23 / AY 2023-24

Please find below a pdf file containing the TDS rates and limits applicable for FY 2022-23/ AY 2023-24.

How to deal with the assessment order passed levying huge tax liabilities, interest and penalty?

Huge add-backs in assessment order? An exemption claim not given? Taxes and interest computed erroneously? Should we file an appeal or not? Penalty order received – wondering what to reply? The order passed in not just and fair?

Are any of these worrying you?

Don’t panic with the huge add-backs, taxes, interest, or penalties raised. Many times orders are passed without considering the facts and law in detail. Many facts and aspects of the law are hidden and if not appropriately pointed out before the tax authorities could lead to orders that are prejudicial to one’s interest. There is more than one remedy available to the taxpayer based on the type of order.

Assessment orders

The orders passed levying huge taxes, interest, etc. could be broadly on account of two reasons:

- Computational errors.

- Disputed issues at hand.

- Computational errors – If the order passed has a mistake that is apparent on record the taxpayer can file a rectification application u/s 154 for the same and need not go for an appeal if there are no disputed issues at hand.

A mistake apparent on record means any mistake which is obvious and patent. The plain meaning of the word “apparent” is that it must be something that appears to be so ex-facie and is incapable of argument or debate. It could be factual errors, mathematical errors, clerical errors, and involuntarily overlooking certain compulsory legal provisions. E.g., the tax percentage taken is erroneous, interest is not computed as per the provisions of the Act, TDS credit has not been given, taxes paid are not considered, deduction, allowance, or relief which is accepted by the officer but overlooked while computing, etc.

Against such mistakes, a rectification application can be filed online u/s 154 and relief be claimed for erroneous computations in the assessment order.

- Disputed issues at hand – if there are issues in the assessment order which are disputed, the remedy in the hands of the taxpayer is to file an appeal with the Commissioner of Appeal in Form 35 within 30 days from the passing of the order. However, for reasons beyond control, an appeal can be filed even after 30 days by filing a condonation of delay application.

How to judge whether one should go for an appeal or not?

The usual errors while passing the Assessment order which could give scope for a good argument and become a significant point in the appeal are as below:

- The order was not passed within the time limit prescribed under the Income Tax Act.

- The order was passed without giving a proper opportunity of being heard.

- Where e- submissions couldn’t be made for technical glitches in portal.

- The video conferencing option requested was not granted.

- The order was passed without giving a prior show cause notice to submit documents or evidence supporting the issues raised by the Assessing Officer.

- The order has been passed by the assessing officer ignoring the facts and documents submitted before them.

- The order passed does not clearly pronounce the issue at hand and has just added back income as unexplained.

- The issue at hand has two opinions and a favorable opinion has been ignored.

- Binding judicial precedents have not been considered while passing the order.

- Additional evidences are present which could not be submitted before the Assessing officer but are crucial in deciding the case at hand.

- Recent amendments/notifications/circulars have not been considered while passing the order.

There could be many such issues, one must take expert advice before filing an appeal to decide whether it’s a fit case to proceed or not.

Form 35 – Crucial Points to be considered

- Prepare a brief Statement of facts covering all facts of the case and also state the facts that are ignored by the assessing officer

- Grounds of appeal – this should ideally cover all the objections raised both from a law and facts perspective with quoting of sections wherever applicable.

- 20% of the disputed demand needs to be paid upfront at the time of filing an appeal.

- Appeal filing fee needs to be remitted before uploading the Form 35.

- Additional evidences if any, which were not submitted before the Assessing officer needs to be mentioned in the statement of facts and in Form 35.

- If an appeal is not filed within the time limit, a condonation application is to be enclosed.

Though the form 35 is available on the portal and one can directly file an appeal, it is always advisable to take professional support as there are many precautions that need to be exercised to avoid further issues while representing the case.

Penalty orders

The penalty orders received need to be responded to within the time limit otherwise huge penalty would be levied. Penalty could be for various reasons such as not filing of returns, non-audit of books of accounts, default in TDS/TCS remittances if income has escaped assessment or contravention of loan provisions etc.

The penal provisions under the Act are very stringent, but irrespective of it the taxpayer will be given an adequate chance to represent and submit all documents and evidence so as to justify why the penalty should not be received.

One should clearly see which section is applicable and what are the conditions to levy penalty under that section. Based on the facts and law one can represent why the penalty should not be levied. Further in cases of genuine hardship caused to the taxpayer one can try to reduce the penalty amount by taking the support of many judicial precedents.

Conclusion

One should not panic looking at the orders passed and taxes levied. Instead, patiently look for points both factually and legally which could justify and get the rightful claim to you. There are various remedies available at the hand of a taxpayer. One needs to exercise the options at the right time and in the right manner to protect their interest.