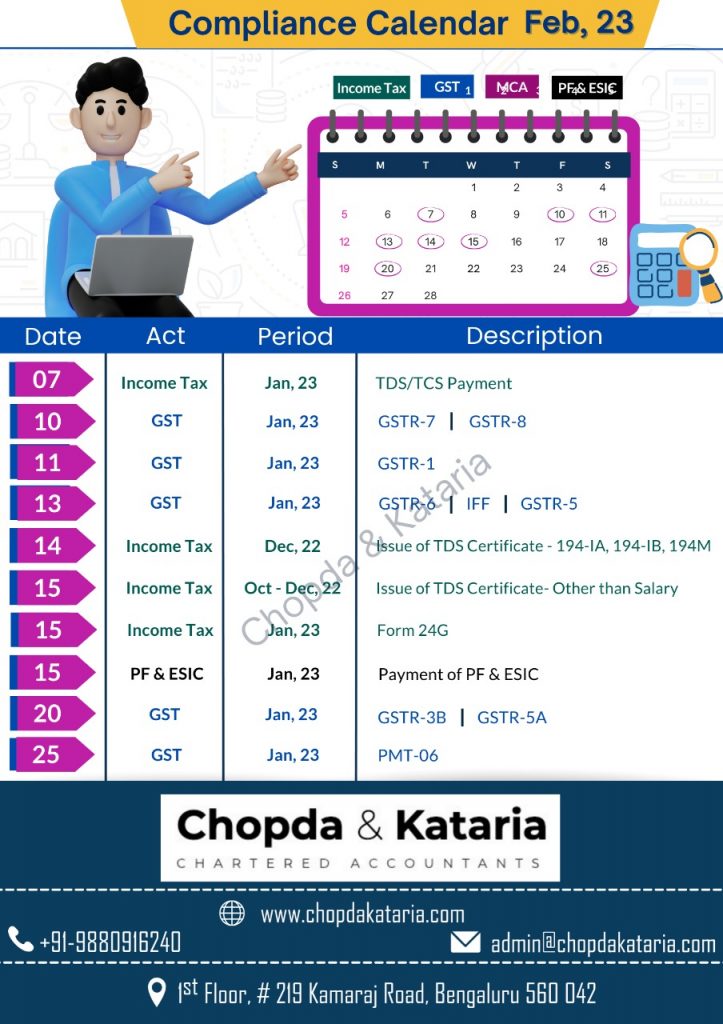

Compliance Calendar for February 2023

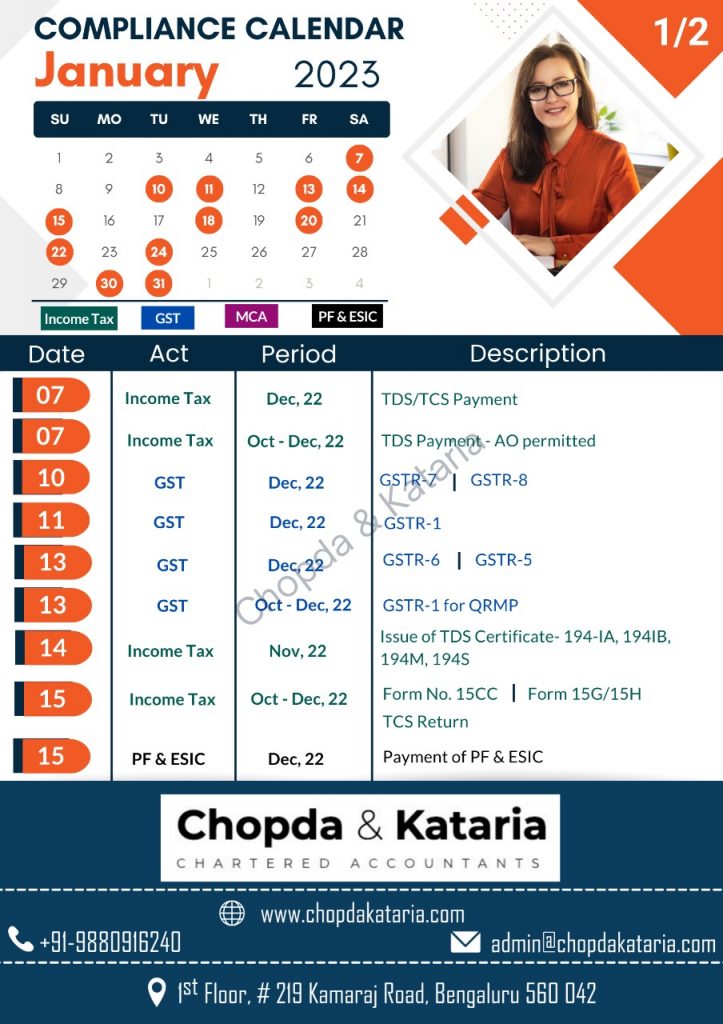

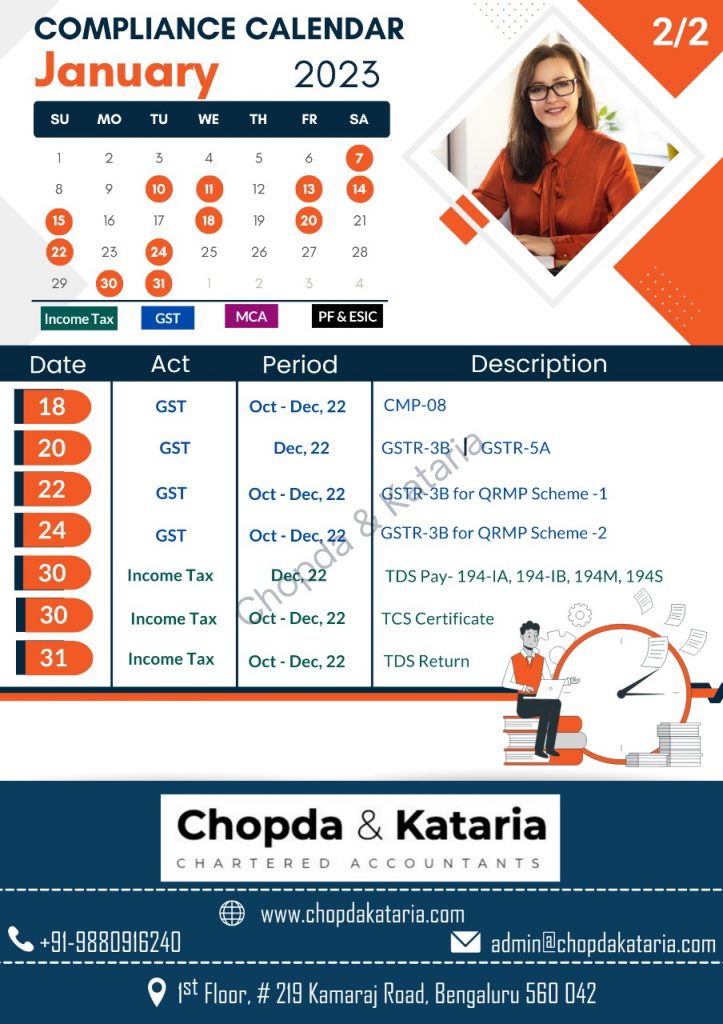

Compliance Calendar for January 2023

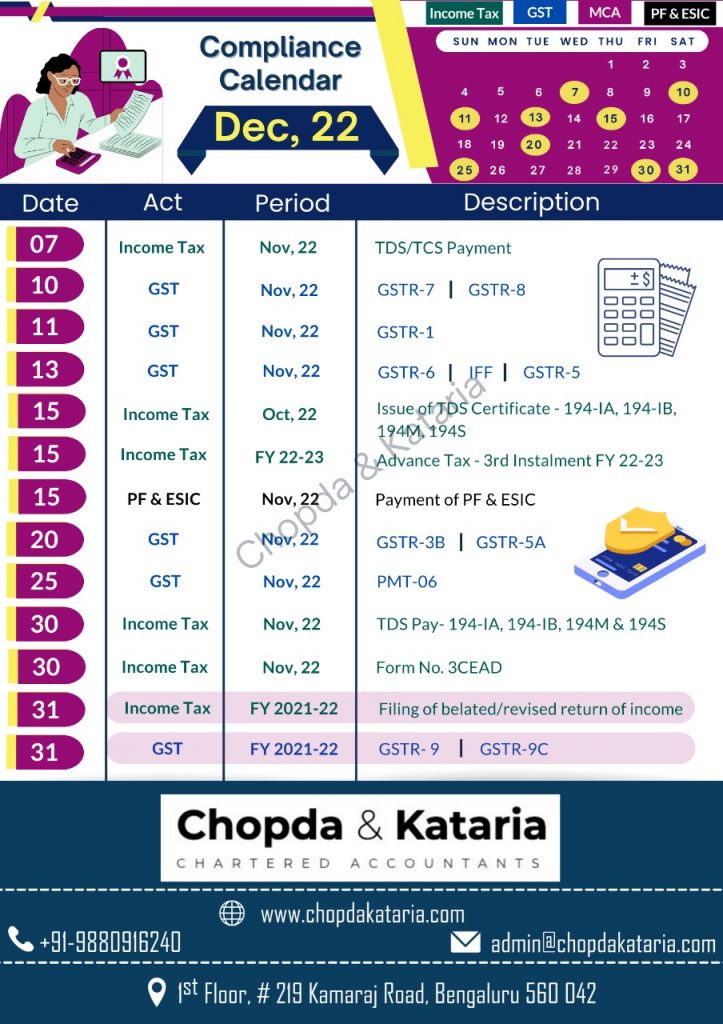

Compliance Calendar for December 2022

TDS Rates and Limits for FY 2022-23 / AY 2023-24

Please find below a pdf file containing the TDS rates and limits applicable for FY 2022-23/ AY 2023-24.

How to deal with the assessment order passed levying huge tax liabilities, interest and penalty?

Huge add-backs in assessment order? An exemption claim not given? Taxes and interest computed erroneously? Should we file an appeal or not? Penalty order received – wondering what to reply? The order passed in not just and fair?

Are any of these worrying you?

Don’t panic with the huge add-backs, taxes, interest, or penalties raised. Many times orders are passed without considering the facts and law in detail. Many facts and aspects of the law are hidden and if not appropriately pointed out before the tax authorities could lead to orders that are prejudicial to one’s interest. There is more than one remedy available to the taxpayer based on the type of order.

Assessment orders

The orders passed levying huge taxes, interest, etc. could be broadly on account of two reasons:

- Computational errors.

- Disputed issues at hand.

- Computational errors – If the order passed has a mistake that is apparent on record the taxpayer can file a rectification application u/s 154 for the same and need not go for an appeal if there are no disputed issues at hand.

A mistake apparent on record means any mistake which is obvious and patent. The plain meaning of the word “apparent” is that it must be something that appears to be so ex-facie and is incapable of argument or debate. It could be factual errors, mathematical errors, clerical errors, and involuntarily overlooking certain compulsory legal provisions. E.g., the tax percentage taken is erroneous, interest is not computed as per the provisions of the Act, TDS credit has not been given, taxes paid are not considered, deduction, allowance, or relief which is accepted by the officer but overlooked while computing, etc.

Against such mistakes, a rectification application can be filed online u/s 154 and relief be claimed for erroneous computations in the assessment order.

- Disputed issues at hand – if there are issues in the assessment order which are disputed, the remedy in the hands of the taxpayer is to file an appeal with the Commissioner of Appeal in Form 35 within 30 days from the passing of the order. However, for reasons beyond control, an appeal can be filed even after 30 days by filing a condonation of delay application.

How to judge whether one should go for an appeal or not?

The usual errors while passing the Assessment order which could give scope for a good argument and become a significant point in the appeal are as below:

- The order was not passed within the time limit prescribed under the Income Tax Act.

- The order was passed without giving a proper opportunity of being heard.

- Where e- submissions couldn’t be made for technical glitches in portal.

- The video conferencing option requested was not granted.

- The order was passed without giving a prior show cause notice to submit documents or evidence supporting the issues raised by the Assessing Officer.

- The order has been passed by the assessing officer ignoring the facts and documents submitted before them.

- The order passed does not clearly pronounce the issue at hand and has just added back income as unexplained.

- The issue at hand has two opinions and a favorable opinion has been ignored.

- Binding judicial precedents have not been considered while passing the order.

- Additional evidences are present which could not be submitted before the Assessing officer but are crucial in deciding the case at hand.

- Recent amendments/notifications/circulars have not been considered while passing the order.

There could be many such issues, one must take expert advice before filing an appeal to decide whether it’s a fit case to proceed or not.

Form 35 – Crucial Points to be considered

- Prepare a brief Statement of facts covering all facts of the case and also state the facts that are ignored by the assessing officer

- Grounds of appeal – this should ideally cover all the objections raised both from a law and facts perspective with quoting of sections wherever applicable.

- 20% of the disputed demand needs to be paid upfront at the time of filing an appeal.

- Appeal filing fee needs to be remitted before uploading the Form 35.

- Additional evidences if any, which were not submitted before the Assessing officer needs to be mentioned in the statement of facts and in Form 35.

- If an appeal is not filed within the time limit, a condonation application is to be enclosed.

Though the form 35 is available on the portal and one can directly file an appeal, it is always advisable to take professional support as there are many precautions that need to be exercised to avoid further issues while representing the case.

Penalty orders

The penalty orders received need to be responded to within the time limit otherwise huge penalty would be levied. Penalty could be for various reasons such as not filing of returns, non-audit of books of accounts, default in TDS/TCS remittances if income has escaped assessment or contravention of loan provisions etc.

The penal provisions under the Act are very stringent, but irrespective of it the taxpayer will be given an adequate chance to represent and submit all documents and evidence so as to justify why the penalty should not be received.

One should clearly see which section is applicable and what are the conditions to levy penalty under that section. Based on the facts and law one can represent why the penalty should not be levied. Further in cases of genuine hardship caused to the taxpayer one can try to reduce the penalty amount by taking the support of many judicial precedents.

Conclusion

One should not panic looking at the orders passed and taxes levied. Instead, patiently look for points both factually and legally which could justify and get the rightful claim to you. There are various remedies available at the hand of a taxpayer. One needs to exercise the options at the right time and in the right manner to protect their interest.

EXTENSION OF TIME LIMITS OF CERTAIN COMPLIANCES UNDER INCOME TAX ACT- REF CIRCULAR NO.9/2021 DATED 20TH MAY 2021.

The Central Board of Direct Taxes, in the exercise of its power under section 119 of the Income-tax Act, 1961 (hereinafter referred to as “the Act”) provides relaxation in respect of the following compliances:

- The Statement of Financial Transactions (SFT) for the Financial Year 202021, required to be furnished on or before 31st May 2021 under Rule 114E of the Income-tax Rules, 1962 (hereinafter referred to as “the Rules”) and various notifications issued thereunder, may be furnished on or before 30th June 2021;

- The Statement of Reportable Account for the calendar year 2020, required to be furnished on or before 31st May 2021 under Rule 114G of the Rules, may be furnished on or before 30th June 2021;

- The Statement of Deduction of Tax for the last quarter of the Financial Year 2020-21, required to be furnished on or before 31st May 2021 under Rule 31A of the Rules, may be furnished on or before 30th June 2021;

- The Certificate of Tax Deducted at Source in Form No 16, required to be furnished to the employee by 15th June 2021 under Rule 31 of the Rules, may be furnished on or before 15th July 2021;

- The TDS/TCS Book Adjustment Statement in Form No 24G for the month of May 2021, required to be furnished on or before 15th June 2021 under Rule 30 and Rule 37CA of the Rules, may be furnished on or before 30th June 2021;

- The Statement of Deduction of Tax from contributions paid by the trustees of an approved superannuation fund for the Financial Year 2020-21, required to be sent on or before 31st May 2021 under Rule 33 of the Rules, may be sent on or before 30th June 2021;

- The Statement of Income paid or credited by an investment fund to its unit holder in Form No 64D for the Previous Year 2020-21, required to be furnished on or before 15th June 2021 under Rule 12CB of the Rules, may be furnished on or before 30th June 2021;

- The Statement of Income paid or credited by an investment fund to its unit holder in Form No 64C for the Previous Year 2020-21, required to be furnished on or before 30th June 2021 under Rule 12CB of the Rules, may be furnished on or before 15th July 2021;

- The due date of furnishing of Return of Income for the Assessment Year 2021-22, which is 31st July 2021 under sub-section (1) of section 139 of the Act, is extended to 30th September 2021;

- The due date of furnishing of Report of Audit under any provision of the Act for the Previous Year 2020-21, which is 30th September 2021, is extended to 31st October 2021;

- The due date of furnishing Report from an Accountant by persons entering into international transaction or specified domestic transaction under section 92E of the Act for the Previous Year 2020-21, which is 31st October 2021, is extended to 30th November 2021;

- The due date of furnishing of Return of Income for the Assessment Year 2021-22, which is 31st October 2021 under sub-section (1) of section 139 of the Act, is extended to 30th November 2021;

- The due date of furnishing of Return of Income for the Assessment Year 2021-22, which is 30th November 2021 under sub-section (1) of section 139 of the Act, is extended to 31st December 2021;

- The due date of furnishing of Return of Income for the Assessment Year 2021-22, which is 30th November 2021 under sub-section (1) of section 139 of the Act, is extended to 31st December 2021;

Clarification 1: It is clarified that the extension of the dates as referred to in clauses (9), (12) and (13) above shall not apply to Explanation 1 to section 234A of the Act, in cases where the amount of tax on the total income as reduced by the amount as specified in clauses (i) to (vi) of sub-section (1) of that section exceeds one lakh rupees.

Clarification 2: For the purpose of Clarification 1, in case of an individual resident in India referred to in sub-section (2) of section 207 of the Act, the tax paid by him under section 140A of the Act within the due date (without extension under this Circular) provided in that Act, shall be deemed to be the advance tax.

TDS RATES FY 2021-22

Please find below a pdf file containing the TDS rates and limits applicable for FY 2021-22 /AY 2022-23.

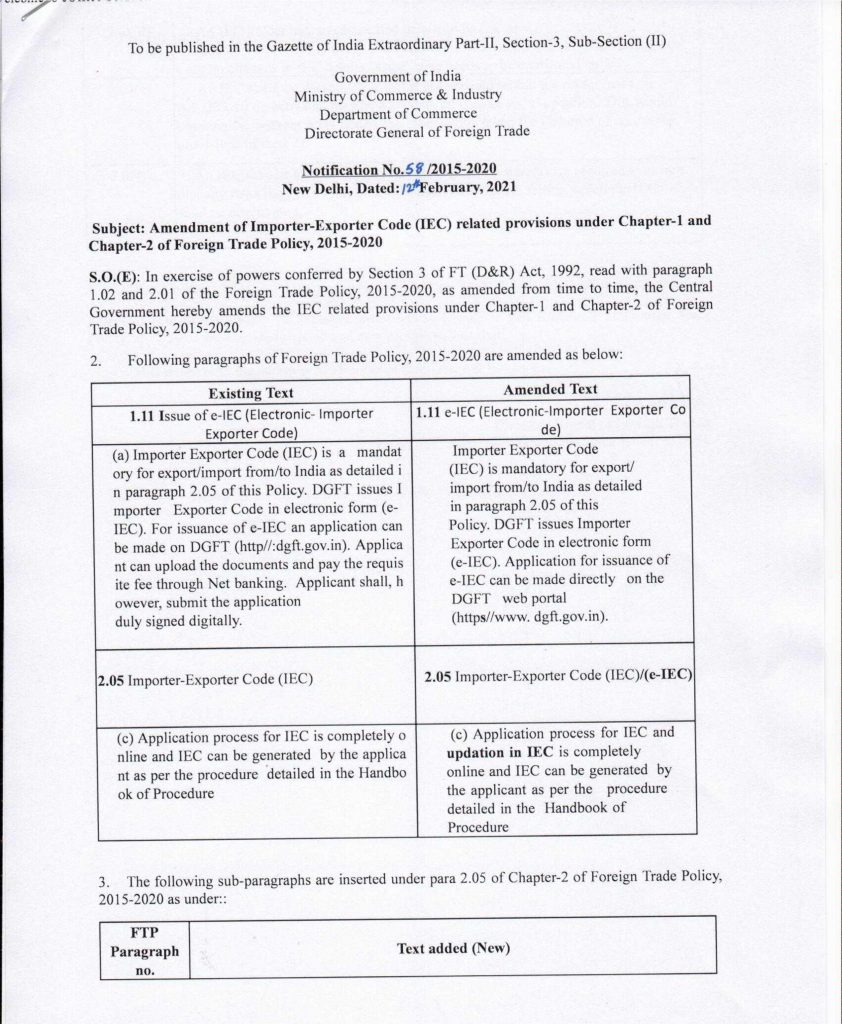

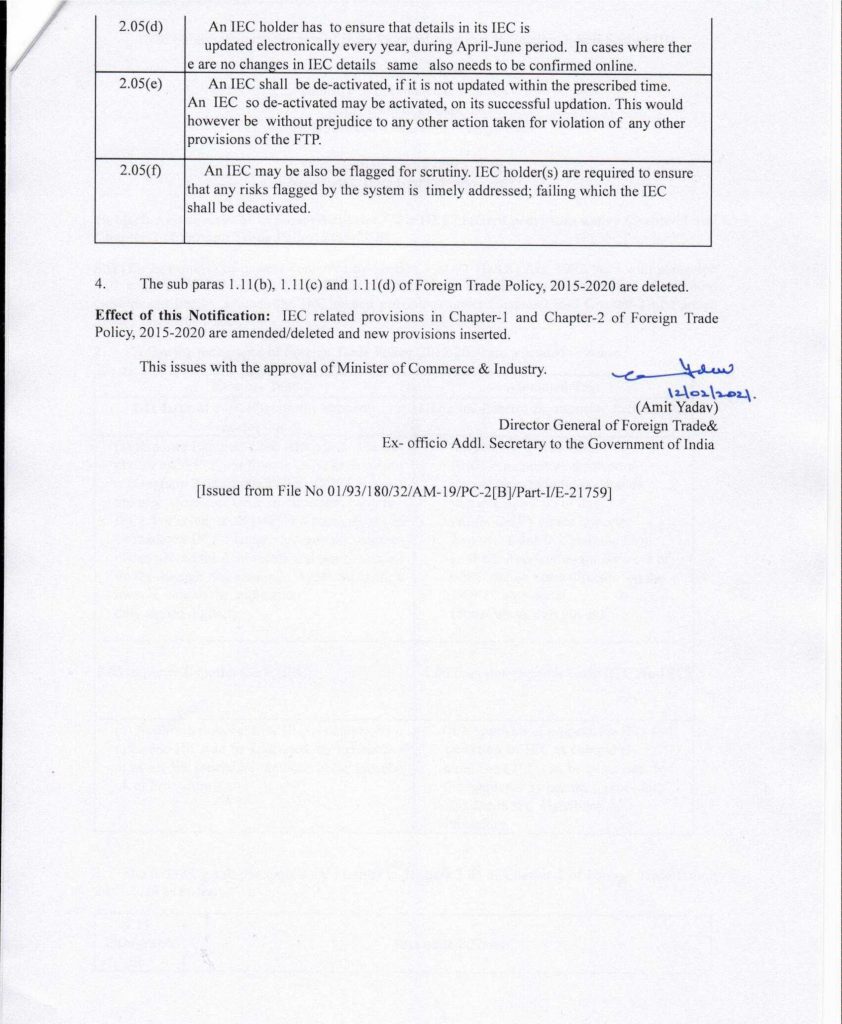

Update Your IEC Yearly or face Deactivation

Background

The Central Government has amended the rules relating to Importer-Exporter Code (IEC) vide Notification No. 48/2015-2020 dated 12 February 2021.

Details of Changes

The notification has introduced additional compliance of a yearly updation of the IEC on importers and exporters, to be done in the months of April – June. A confirmation would be required even if there are no updates/changes to the IEC.

In the event the updation activity is not done within the prescribed time by a business, the same will be deactivated without prejudice to other actions in law, including under the Foreign Trade (Development & Regulation) Act, 1992.

Comment

This additional requirement should be carefully adhered to by businesses, as any non-compliance will result in a deactivation of the IEC and a stop to all import-export activity resulting in severe business losses.

The notification copy is below:

HUF – Tax Planning Tool

What is Hindu Undivided family?

Hindu undivided family (HUF) is a Joint Hindu family with common ancestors. The Hindu Succession Act, defines a HUF, as a family of persons lineally descended from a common ancestor and related to each other by birth or marriage.

In other words, three conditions need to be satisfied:

- Must be a Hindu. The word Hindu for the purpose of having a HUF is construed liberally and includes Jains, Sikh, and Buddhists.

- There should be a family i.e. a group of persons.

- Have common ancestors among them.

Who can be the Karta, Coparcener or a Member of an HUF?

Karta is the person who manages or represents the HUF and is generally the senior-most male member of the family. Only a Co-parcener can become the Karta of HUF.

Any person (male or female) born in a Joint Hindu family who is within four degrees in lineal descendent from the common male ancestor is considered as a coparcener and anyone who becomes part of the family by virtue of marriage is treated as a member. However, a person who is adopted into the family also becomes its coparcener from adoption though not born in the family. As per the amended law since 2005, even a girl child becomes a coparcener by birth and can continue to be a co-parcener of her father’s HUF even after her marriage. However, she will only be a member of her husband’s HUF.

Co-parceners have a right to seek partition and become the Karta of the HUF. Whereas, Members have the right to be maintained out of the funds of HUF, and receive their share at the time of partition but do not have the right to seek for partition or become the Karta.

How taxed under Income tax Act.

The Income-tax Act recognizes such family as a separate entity. The definition of ‘person’ under section 2(31) of the Income Tax Act 1961 includes HUF as a separate person having its own status, distinct from any individual, firm, company, etc. A HUF is created by the operation of law and therefore cannot be created by the actions of a person.

How to create a HUF

HUF comes into existence automatically at the time of marriage. It is created through executing a deed, obtaining PAN, and applying for a bank account. The various source of its assets could be:

- By way of gift

- By Will

- Common Ancestral property

- Property acquired from the sale of joint family property

- Property contributed to the common pool by members of HUF.

Note: To ensure personal assets or funds are not transferred to HUF account as income generated from such assets/funds will attract clubbing provisions.

How creating of HUF helps save tax legally

HUF is considered a separate legal entity as per law and hence has its own PAN and files tax returns independent of its members. By forming a HUF, one can optimize their tax liabilities and also include their family members to benefit in the future. The various advantages are:

- Deductions and exemptions

A HUF is taxed at slab rates – the same rate as that of an individual and is eligible for a basic tax exemption limit of Rs 2,50,000.

HUF is also separately eligible for various deductions under section 80 such as:

- Deductions for specified investments under section 80C in LIC, PPF, NSC, etc., up to Rs 1,50,000 every year.

- Mediclaim for its family members under section 80D up to Rs 30,000.

- Interest on savings accounts u/s 80TTA up to Rs 10,000.

Thus, total deduction of Rs 1,90,000 could be availed by the HUF irrespective of its individual member deductions.

Further specific deductions on medical treatment/expenditure of disabled or dependent family members, donations to charity, etc can be availed based on the amount spent for the said purposes.

- House property benefits

- Rental income could be received on behalf of HUF, instead of the individual account.

- The HUF is also entitled to claim a deduction for interest on self-occupied house property of Rs. 2,00,000 in a year.

- If residential house property is purchased by the HUF, the home loan interest paid and repayment of the loan can be claimed as a deduction.

- The HUF can also let out its property to any person and interest on loan paid deduction can be availed without any limit, in respect of the said property.

- Business income

The HUF can carry on certain family business like any other entity:

- Profits generated out of the family business, in the name of a HUF, shall be taxed accordingly and exemptions will give more leverage on tax saving.

- It can pay remuneration to Karta and other family members.

- Can give loans to its members

- Investments and capital gain exemptions

The HUF is permitted to invest in various tax-free instruments. Also, it can avail specific capital gain exemptions under sections 54, 54B, 54F, 54EC, etc., and optimize its tax liabilities for the benefit of the entire family.

- Family Settlement or Arrangement:

The sole purpose of the family settlement should be to settle existing or future disputes regarding property, amongst the members of the family. Since this arrangement does not involve the transfer, it would not attract gift tax, capital gains tax, or clubbing. In a family arrangement, tax incidence is considerably reduced or it may even become nil.